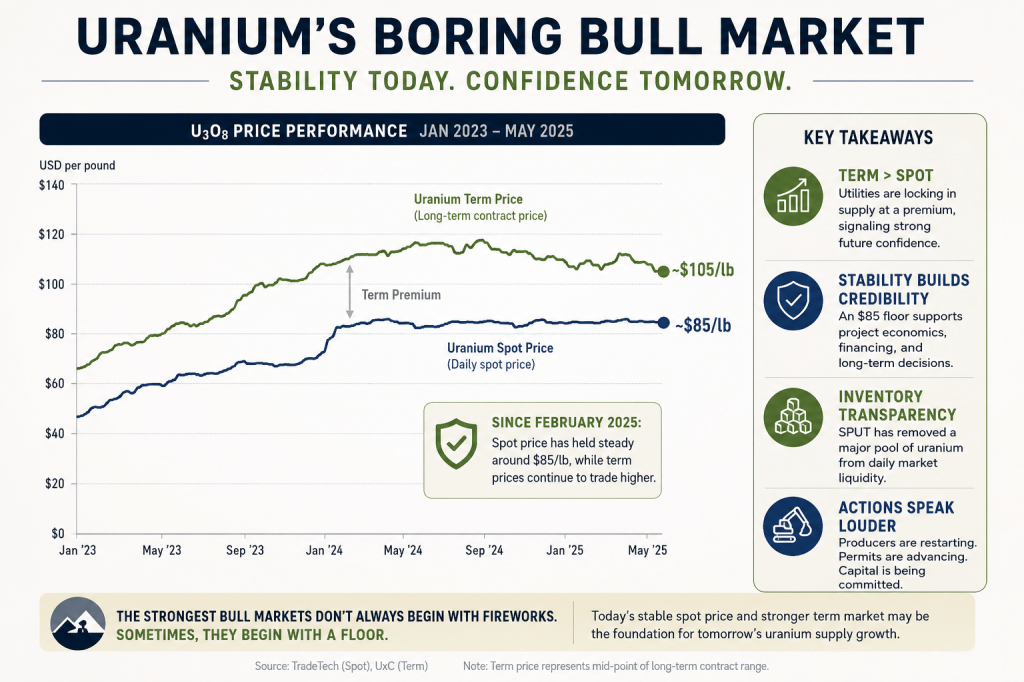

Why an $85 Spot Price May Matter More Than the Next Price Spike

For nearly five months, the uranium market has done something unusual.

Not much of anything.

Since roughly February, spot uranium has parked in the mid-$80s per pound. Investors who remember the fireworks of past cycles might read that as a letdown. Commodity markets are supposed to move. Bull markets are supposed to roar. Headlines are supposed to chase new highs.

Instead, uranium has gone quiet.

That quiet may turn out to be one of the strongest bullish signals this market has produced in years.

As a geologist, I spend far less time forecasting prices than I do judging whether projects can actually get built. Markets are interesting, but geology eventually has to meet engineering, permitting, financing, and execution. A deposit that only works at $140 uranium is a bet on the future. A deposit that works at $80–90 uranium is starting to look financeable.

That difference matters.

The Spot Price Isn’t the Uranium Market

One of the most common mistakes investors make is treating the spot price as if it were the whole market.

It isn’t.

Unlike gold, copper, or oil, most uranium changes hands through long-term contracts negotiated directly between producers and utilities. Spot transactions account for only a small slice of annual volume. Spot matters because it’s visible — but it’s not where most nuclear fuel actually gets bought.

The term market is where utilities lock in supply years in advance. Those contracts decide whether new mines get financed, idled mines restart, and development projects graduate from slide decks to production schedules.

Spot reflects today’s mood.

Term reflects tomorrow’s confidence.

Right now, confidence appears to be running well ahead of the spot price.

Why Stability Matters

Commodity traders love volatility. Mine developers do not.

Picture underwriting a uranium project where spot sits at $85 today but could just as easily land at $55 next year. Financing gets harder. Mine plans get more conservative. Investors get cautious.

Now picture the alternative.

Spot holds steady near $85 through shifting sentiment, geopolitical noise, speculative flows, and the usual seasonal chop.

That kind of stability builds something more valuable than a temporary price spike ever could: credibility.

Boardrooms start evaluating projects on firmer footing. Banks start underwriting cash flows with more confidence. Technical reports lean less on optimistic pricing assumptions and more on a market that looks durable.

No serious engineer builds a mine around peak commodity prices. Everyone wants a floor they can count on.

What the Term Market Is Quietly Saying

The most telling feature of today’s uranium market isn’t the spot price — it’s the gap between spot and term.

Utilities keep signing long-term contracts above where spot sits today.

That spread is a signal.

Utilities aren’t buying uranium for next quarter. They’re securing fuel for reactors that will still be running years — often more than a decade — from now.

When buyers are willing to pay a premium over today’s visible price, they’re signaling a willingness to pay down future supply risk now.

Behavior often says more than headlines. Right now, it’s the utilities doing the talking.

SPUT Changed the Conversation

A few years ago, talk of uranium inventories was mostly guesswork.

Everyone knew material sat in warehouses, government stockpiles, utility reserves, and commercial holdings — but almost none of it was visible. The question never changed: how much uranium is actually available to buy?

The Sprott Physical Uranium Trust changed that.

For perhaps the first time in the uranium market’s history, one of the largest holders of physical uranium publicly discloses exactly how many pounds it owns.

Those pounds aren’t ordinary trading inventory. Barring a major structural shift, uranium held by SPUT is effectively pulled out of day-to-day market liquidity.

That doesn’t settle every inventory question. Utilities still hold reserves. Governments maintain strategic stockpiles. Producers retain working inventories. Traders hold material. Other investment vehicles exist too.

But SPUT turned one meaningful part of the inventory discussion from guesswork into arithmetic. It doesn’t answer the broader inventory question, but it gives far more visibility into one of the largest pools of investment-held uranium than the market has ever had.

That’s real progress.

A Price Floor Changes Behavior

One consequence of a stable uranium market gets surprisingly little attention: price floors change behavior.

Developers become more willing to advance projects. Lenders become more comfortable underwriting capital. Utilities become more willing to contract years out. Investors start evaluating companies on project quality rather than simply waiting for higher commodity prices.

Stability itself becomes part of the investment thesis.

The market doesn’t need euphoria to attract investment. It just needs to be dependable enough that participants can make long-term decisions with confidence.

Actions Speak Louder Than Prices

The strongest evidence behind this market isn’t on a price chart. It’s in what companies are doing.

Across the United States, uranium producers are restarting operations, advancing permits, running processing campaigns, and pulling long-dormant projects back toward production.

Capital is being committed. Permits are moving. Infrastructure is being rebuilt.

Executives aren’t making these calls because they expect spot to jump five dollars next week. They’re making them because they increasingly believe today’s prices support the economics of a mine over its full life.

That’s a fundamentally different mindset than the one that dominated just a few years ago.

Geology Doesn’t Need Excitement

Exploration geologists learn early that spectacular results get outsized attention — the highest-grade intercept, the richest assay, the headline discovery.

But great mining districts aren’t built on isolated spectacular results. They’re built on consistency.

Commodity markets aren’t all that different.

An orderly market — built on disciplined contracting, realistic economics, greater inventory transparency, and steady production growth — may ultimately prove healthier than another speculative spike followed by another crash.

Investors chase excitement. Developers chase confidence. Those aren’t always the same thing.

Beyond the Headlines

Could uranium prices move substantially higher? Certainly. Growing electricity demand, reactor life extensions, new nuclear construction, and constrained mine supply all support a constructive long-term outlook.

But the more interesting question may not be how high uranium prices can go. It may be whether today’s prices are already durable enough to finance tomorrow’s mines.

If they are, the recent quiet isn’t a sign of weakness. It may be the market telling us something bigger: uranium is becoming investable, financeable, and buildable.

The strongest bull markets don’t always begin with fireworks.

Sometimes they begin with a floor.