Something big just moved beneath the surface—and not just geologically.

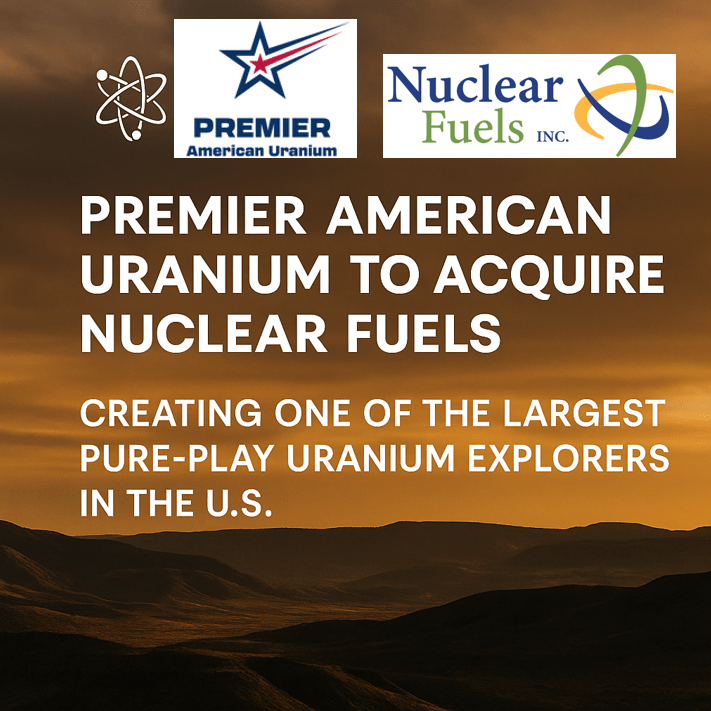

On June 5th, it was announced that Premier American Uranium Inc. (PUR) will acquire Nuclear Fuels Inc. (NF), creating one of the largest pure-play uranium explorers in the United States. As someone who’s had the privilege of serving as Project Manager for Nuclear Fuels, I’m proud to share that this is not the end of a chapter—it’s the doubling down of a mission. And I’ll continue to be actively involved in this newly merged entity as we push forward across the map, the drill deck, and the development pipeline.

What This Means: Consolidation with Purpose

The new company brings together:

- 12 exploration and development-stage projects across Wyoming, New Mexico, Utah, Arizona, and Colorado;

- A land position totaling over 104,000 acres;

- Historic and modern datasets from more than 4,200+ drill holes in Wyoming alone;

- And a rare emphasis on ISR-focused uranium exploration, an area often overlooked but critically needed for the U.S. energy transition.

This isn’t consolidation for consolidation’s sake. It’s strategic integration—combining NF’s flagship Kaycee Project in Wyoming’s Powder River Basin with PUR’s Cyclone Project in the Great Divide Basin, both sitting squarely within America’s most prolific ISR districts.

Why Now? Because Timing is Everything

We’re in a moment.

In the last few months alone:

- Uranium projects in the U.S. are being fast-tracked.

- The Grants Mineral Belt in New Mexico—home to PUR’s Cebolleta Project—has received federal attention via the FAST-41 permitting program.

- And domestic supply security has become more than a talking point—it’s a mandate.

This merger lands at exactly the right time, with exactly the right assets, and exactly the right team.

Kaycee: A Keystone Asset

Let me take a moment to highlight what makes Kaycee so special—because I’ve walked it, mapped it, and logged more than a few of those holes myself.

Kaycee spans a 35-mile roll-front system with over 430 miles of mapped trends, supported by historic drilling and modern work that proves uranium mineralization in all three major sand units: Wasatch, Fort Union, and Lance. That’s a rarity in ISR uranium, and it’s a big part of why this deal makes so much sense.

Our 2023 and 2024 drill campaigns were among the largest ISR exploration programs in the U.S., and the trend is just beginning to heat up. With C$14M in combined cash on hand, the new company is poised to aggressively advance Kaycee and our other high-potential assets in the months to come.

The People Behind the Rocks

This isn’t just about drill footage and roll fronts.

The combined company will be backed by some of the strongest strategic players in the space—Sachem Cove, enCore Energy, IsoEnergy, and Mega Uranium—and led by Colin Healey as CEO, with representation from both the PUR and NF boards. I’m honored to remain involved post-merger, contributing to the continued growth of the project portfolio and the technical strategy that guides it.

Exploration geologists don’t often get to see their work reach critical mass. This is one of those rare and exciting exceptions.

Looking Ahead

U.S. uranium isn’t just coming back. It’s growing smarter. Sharper. More deliberate.

With the Premier-Nuclear Fuels merger, we’re not just stitching together acreage. We’re assembling the kind of exploration-first, production-ready platform that’s been missing from the domestic uranium narrative. A platform with the data, the drilling history, the land, the resources—and the team—to make something enduring.

This is about more than uranium. It’s about how we meet the energy future with boldness, science, and a little bit of grit.

🔗 If you’re following the uranium sector, the time to pay attention is now. If you’re already invested—in industry, interest, or curiosity—this is a story worth tracking.

And if you’re a geologist like me?

You know what this really means: we’ve still got plenty of ground to cover—and we’re just getting started.