The U.S. Nuclear Regulatory Commission is reorganizing.

On the surface, that sounds bureaucratic. Org charts. Reporting lines. Internal memos.

But don’t be fooled.

This may be one of the most consequential structural signals for nuclear energy — and uranium — in decades.

What’s Actually Happening?

The U.S. Nuclear Regulatory Commission is restructuring around three core business lines:

New Reactors

Operating Reactors

Nuclear Materials & Waste

Licensing and inspection functions will be integrated. Accountability will be centralized within each line. Decision velocity is the objective.

This is not deregulation.

This is reorganization for efficiency.

And efficiency, in nuclear, has historically been the missing variable.

From Fear to Function

There was a time when America built reactors.

Under the United States Atomic Energy Commission, nuclear power was both regulated and promoted — sometimes imperfectly, but with ambition.

Then came the era of public fear, media amplification, and institutional risk aversion. The China Syndrome premiered. Three Mile Island accident followed.

Permitting paradigms hardened. Timelines stretched. Capital retreated.

The industry didn’t die. It slowed.

This reorganization signals something different:

A regulator aligning itself with national deployment goals — without abandoning safety.

That distinction is everything.

The Elephant in the Room: Uranium

If the NRC becomes faster, clearer, and more accountable in licensing new reactors, the consequences ripple upstream immediately.

Amir Adnani, CEO of UEC, has floated the possibility of $1,000/lb U₃O₈ in a true supply squeeze (at a recent talk given in Vancouver (VRIC 2026)).

Is that the base case? No.

But the direction of travel matters more than the ceiling.

When regulatory friction decreases, capital confidence increases. When capital confidence increases, projects move. When projects move, supply tightens against accelerating demand.

This is how structural bull markets are born.

Unlocking the Upstream

For uranium producers and explorers, a credible acceleration in nuclear deployment does several things:

Unlocks equity financing for restarts and greenfields

Encourages long-term utility contracts

Justifies domestic enrichment and conversion build-out

De-risks jurisdictional narratives

But here’s the deeper layer:

Regulatory reform does not just unlock production.

It unlocks exploration.

And exploration is where the real asymmetry lives.

Humanity’s New Fire

Nuclear energy is not just another commodity cycle.

It is 3,000,000-to-1 energy density. It is grid stability in an AI-powered century. It is geopolitical leverage. It is decarbonization without fragility.

It is Prometheus without smoke.

If the NRC reorganization proves durable — if it translates into measurable timeline compression — then we are not witnessing a bureaucratic shuffle.

We are witnessing the quiet removal of a bottleneck.

And when bottlenecks disappear, abundance flows.

Where I Stand

In a world where regulatory velocity meets capital discipline, the most valuable role is not the driller or the promoter.

It is the translator.

The one who stands between geology, permitting, and capital and asks:

Is this technically real?

Is this jurisdictionally viable?

Is this capital-ready?

Is this timed correctly within the cycle?

That’s the lane I operate in.

Because when humanity reaches again for its new fire, someone must ensure the spark lands where it can actually burn.

This NRC reorganization may seem administrative.

But to those watching the full arc — from regulator to reactor to uranium to discovery —

How Modular Processing Is Rewriting the Economics of Complex Ore Systems

Something fundamental has shifted in how the United States is thinking about minerals—and it didn’t start with a mining company.

It started with the U.S. Army.

In December, Reuters reported that the U.S. military is actively developing small, modular refineries for critical minerals, beginning with antimony and potentially expanding to other strategically essential elements. These are not conceptual studies or policy white papers. They are physical facilities—designed to be compact, deployable, resilient, and secure.

Let that reality settle in.

The U.S. military is no longer assuming that global processing markets will be there when it needs them. It is no longer content to rely on foreign refining capacity for materials essential to defense, technology, and national security. Instead, it is moving processing closer to home—and deliberately shrinking the scale at which it must occur.

That single decision quietly rearranges the board.

Because once processing can be modular, localized, and purpose-built, a whole class of deposits long written off as “too hard” suddenly demands a second look.

Why Antimony Matters—and Why It’s Just the Beginning

The choice of antimony as the starting point is not accidental. Antimony is critical for ammunition, alloys, flame retardants, and a range of defense applications. Yet the United States is almost entirely dependent on foreign refining capacity, with China dominating global processing.

At nearly the same moment, Perpetua Resources announced a partnership with Idaho National Laboratory to build a domestic antimony processing facility tied to the Stibnite project—explicitly framing metallurgical capacity as a matter of national security rather than just mining economics.

Taken together, these moves signal something deeper than a single metal or project. They represent a recognition that processing itself—not just mining—has become strategic infrastructure.

These are not isolated developments. They are load-bearing beams.

The Quiet Inversion of Value

For decades, mineral exploration carried a quiet graveyard of ideas.

Districts left behind. Deposits labeled uneconomic. Projects shelved not because the geology failed—but because the metallurgy did.

They were too polymetallic. Too complex. Too awkward for clean flowsheets and tidy concentrates. Penalty elements loomed. Recoveries weren’t elegant. And by the standards of their time, the economics never quite cleared the bar.

But geology, like history, has a way of reworking old material under new conditions.

What we are witnessing now—almost beneath the noise of quarterly earnings calls and policy press releases—is a structural inversion of value. The very attributes that once doomed complex ore systems are becoming the reasons they matter.

This is the critical minerals framework at work.

Criticality isn’t about elegance. It’s about vulnerability.

When Processing Stops Being a Liability

For much of modern mining history, success meant fitting neatly into an existing industrial mold: single-commodity recovery, conventional flotation, and concentrates that slid smoothly into global smelter networks.

Anything outside that template was discounted, deferred, or abandoned.

But once processing becomes localized, modular, and strategic, the logic flips.

Polymetallic systems—especially carbonate replacement deposits (CRDs) across Nevada and the broader Great Basin—often host exactly the element suites now appearing on critical minerals lists: antimony, zinc, lead, copper, silver, bismuth, arsenic pathfinders, and more.

What used to be metallurgical “noise” becomes strategic signal.

Complexity no longer disqualifies a deposit. In some cases, it enhances it.

Nevada’s Second Act

Consider historic silver or strategic-metals districts in the Great Basin and other polymetallic systems scattered across Nevada.

Historically, they faced familiar headwinds: multiple metals complicating recovery, elements that triggered smelter penalties, and project scales that struggled to justify bespoke processing solutions. In previous cycles, that complexity pushed them to the margins.

Under today’s conditions, those same attributes begin to look different.

Multiple metals become optionality rather than burden. Complex metallurgy becomes leverage rather than liability. Domestic processing capacity becomes a priority rather than an afterthought.

The emergence of small-scale, modular refining—whether military-led, government-assisted, or public–private—reshapes the economic calculus. Not every district reopens overnight. Not every deposit becomes viable. But the door that was once bolted shut is now undeniably open.

Mining as Remediation, Not Relic

There is an uncomfortable truth the broader conversation often avoids: the best way to clean up legacy mine sites is to mine them again—properly.

Modern mining is not the mining of the past. Today’s operations rely on precision drilling, advanced modeling, closed-loop water systems, electrified fleets, and far tighter environmental controls.

Abandoned sites do not heal themselves. They oxidize, leach, erode, and persist.

Responsible redevelopment isn’t regression. It’s reclamation with intent—and with a business plan.

The System Assembles

Step back far enough and the pieces begin to interlock.

Mining produces the metals that feed battery supply chains. Batteries electrify mining fleets and industrial equipment. Nuclear power delivers dense, reliable, carbon-free energy. Critical minerals underpin AI, defense systems, and grid resilience. Domestic processing closes the loop.

This isn’t contradiction. It’s recursion.

Mining metals to build batteries that power mining equipment, fueled by nuclear energy, to produce the materials that sustain a low-carbon, high-technology civilization.

Yes, it means more mining. But it also means smarter, cleaner, more intentional mining—guided by geology, enabled by technology, and reinforced by national strategy.

The Real Keystone

The lynchpin isn’t a single policy, deposit, or refinery.

It’s the recognition that complexity is no longer a flaw.

What was once “too hard” is now too important to ignore.

And in that realization lies the reopening of forgotten districts, the revival of overlooked systems, and perhaps the foundation of the next industrial era—one where geology, technology, and security finally pull in the same direction.

Civilization runs on minerals. Gold may glitter, but copper carries our current, uranium powers our grids, and rare earths anchor the very magnets that spin the world. Without them, the skyscrapers don’t rise, the phones don’t ring, and the servers that feed the cloud go dark. Mining is not just an industry; it is the bedrock upon which every other modern enterprise rests.

And yet, here we stand in 2025, after more than a decade of neglect. The global mining industry has starved its own “R&D department”—exploration. Budgets have been slashed, geologists retired without replacement, and entire districts left unmapped since the 1980s. Instead of planting seeds for the future, the sector has lived off old harvests, leaning on deposits discovered by the last great exploration wave of the 1960s–1990s.

It’s the equivalent of eating the seed corn to make it through winter. Yes, you may survive the lean season, but when spring arrives the fields are bare. The industry now faces a generational dilemma: demand is rising with electrification, AI-driven power consumption, and defense needs, but the pipeline of new discoveries is running dry.

The warning signs are already here. Grades are falling, permitting timelines stretch a decade or more, and the very talent pool of geologists—the human capital that finds ore before machines can mine it—is shrinking. The exploration torch is passing out, just as the world needs it most.

This is the seed corn problem: an industry that mistook austerity for efficiency, cost-cutting for strategy, and in doing so mortgaged its future.

Why Exploration Matters

Exploration is the ghost in the machine—the unseen force that keeps the gears of civilization turning. Mines are not infinite. Ore bodies deplete, grades decline, and production costs inevitably climb. Without a steady stream of new discoveries, the reserves that underpin our supply chains wither away.

When exploration falters, the ripple effects are immediate and profound:

Depletion at the source: Mature mines close or shift to lower-grade zones, requiring more energy, more water, and more waste rock for every ton of metal produced.

Fragile supply chains: Scarcity tightens the noose. Nations grow dependent on single suppliers or unstable jurisdictions, inviting shortages and geopolitical choke points.

Economic exposure: Industries that appear cutting-edge—AI, data centers, quantum computing, crypto, electric vehicles, wind turbines, solar panels—become castles built on sand, unsupported by the very raw materials that make them possible.

History proves the point. The U.S. uranium boom of the 1950s, the global porphyry copper discoveries of the 1960s and 1970s, and the Carlin Trend gold rush in Nevada all reshaped economies and societies. But each relied on bold, boots-on-the-ground exploration—and each took decades to bring from discovery to production. Without planting new seeds today, there will be no harvest tomorrow.

Exploration is not optional. It is the bedrock of resilience, the insurance policy against scarcity, and the quiet act of faith that there will still be metal in the mill when the world comes calling.

What Happened to the Juniors?

Once, junior explorers were the daring prospectors of capital markets. They were scrappy, nimble, and driven by geologists with calloused hands and big dreams—funded by retail investors and risk-tolerant funds who saw the outsized upside of a drill-bit discovery. They were the seed planters.

Today, they’re skeletal. The ecosystem that once sustained them has been hollowed out by a perfect storm of mistrust, market shifts, and changing appetites for risk.

Burned Trust (2011–2015): Billions vanished in the last gold cycle. Over-promises, bad geology, and outright scams poisoned the well. Investors fled, leaving legitimate juniors to starve alongside the frauds.

ETF Domination: Passive index funds became the new custodians of capital. They allocate by market cap, not by exploration potential. Drill holes don’t move the needle. The capital pool that once flowed freely into high-risk discovery stories has shrunk to a trickle.

Retail Drift: The everyday investor who once bought a thousand shares of a penny-stock explorer on a hunch now chases tech IPOs, cannabis booms, meme stocks, and crypto tokens. Rocks lost their shine in a world of instant returns and digital buzz.

Risk Aversion: Institutional capital demands cash flow, not speculation. Money flows to mid-tiers and majors who can produce quarterly results, not to juniors who burn cash in search of something that may not exist.

The result? An entire generation of junior companies reduced to husks—managing legacy properties, eking out survival on private placements, or vanishing altogether. Where once the TSX-Venture exchange was a bustling bazaar of discovery, it is now a thinly traded echo chamber.

The juniors are left begging for scraps. And without them, the pipeline of new discoveries—the very seed corn of the mining industry—runs dry.

Why the Majors Look Away

Big mining companies are not innocent bystanders in this drought of discovery. They’ve made a calculated choice—a choice that prioritizes quarterly comfort over generational security.

Dividends > Drills: Shareholders demand yield, not uncertainty. The likes of BHP, Rio Tinto, and Vale trumpet their dividend programs as proof of “discipline,” funneling billions back to investors instead of into the geologists who might find tomorrow’s ore bodies. The City of London and Bay Street cheer, but the exploration pipeline withers.

M&A Is Easier: Why risk the cost and uncertainty of greenfield exploration when you can let juniors shoulder the burden and then swoop in later? Barrick, Newmont, and Anglo American have built portfolios on acquisitions rather than discoveries, paying premiums for ounces once desperation sets in. This strategy works only as long as juniors exist—and today, even that seedbed is failing.

Permitting Pain: In the U.S., a new mine can take 10–15 years to permit. In Chile, Peru, and Argentina, political shifts and social unrest regularly derail development. Even Canada, once a paragon of mining stability, has bogged down in federal-provincial wrangling. To the majors, exploration feels like wasted effort if politics can veto production. Why drill if a discovery just becomes a stranded asset?

Artificial Scarcity: A tighter project pipeline props up higher commodity prices. For majors, scarcity is profitable—at least in the short run. Copper prices hold stronger when new supply is uncertain. Uranium equities rally when no new projects are breaking ground. But this “discipline” is short-sighted. Artificial scarcity enriches today’s balance sheets while mortgaging tomorrow’s grids.

The majors’ restraint looks like prudence, but in truth, it is systemic neglect. They have mistaken risk aversion for strategy. Instead of seeding the next generation of mines, they are cannibalizing the last generation’s discoveries, hoping someone else will do the dirty work of prospecting.

Yet “someone else” no longer exists. The juniors are starved, governments are paralyzed, and the majors have parked their drills. The system is eating itself.

The Timeline of Consequences

The story of exploration neglect is not abstract. It unfolds on a clock, with milestones as predictable as they are dire. Here’s what we will see in the coming year, 5 years, and 10 years if this pattern of neglect is allowed to continue:

📍 1 Year (2026): The Plateau(if this isn’t already the case)

Reserves continue to shrink across commodities—global copper reserves, for example, are already skewed toward lower-grade porphyries that cost twice as much to mine as their predecessors.

Senior geologists retire, taking with them decades of local knowledge about belts in Nevada, the Andes, and the African Copperbelt. Their field notebooks, often never digitized, gather dust in basements.

Once-vibrant districts—like northern Ontario’s greenstone belts or the Carlin Trend in Nevada—begin to lose their intellectual “muscle memory.” The living knowledge that connects old drill logs to new targets vanishes.

📍 5 Years (2030): The Gap

Project pipelines hollow out. The majors’ development schedules, already thin, collapse into a handful of advanced brownfield expansions.

Juniors consolidate into survival mergers or collapse outright, leaving only a skeletal handful of companies with active drills. The TSX-Venture—the historical cradle of global discovery—is reduced to a backwater of shell companies and recycled management teams.

Governments scramble to reverse decades of neglect: Washington floats “Critical Mineral Moonshots,” Brussels pushes exploration tax credits, Beijing doubles down on African offtake agreements. But the measures are too late. You cannot conjure ore bodies with subsidies once the drills have gone silent.

Supply deficits bite. Copper, lithium, and rare earths become the new oil shocks—triggering inflation, power rationing, and trade wars over who gets the last shipments.

📍10 Years (2035): The Ghost Tap

You cannot turn on a tap that isn’t connected to a pipeline. Mines take 10–20 years to permit and build. By 2035, the missing decade of exploration has come due.

Critical minerals are no longer market stories—they are national security flashpoints.

China leverages its dominance in rare earths to dictate terms in global trade.

The U.S. Defense Department stockpiles uranium and cobalt like Cold War-era oil.

Europe, unable to build batteries without imported lithium, faces rolling blackouts and stalled EV adoption.

Even record-high commodity prices won’t matter. A $15,000/t copper price or $200/lb uranium price won’t magically materialize new deposits. Discovery takes decades, and the decade has already been lost.

The result is a ghost system: idle smelters, shuttered gigafactories, and stalled wind and solar farms—technology stranded for want of the materials that should have been planted years before.

The Geopolitical Context

We are entering an era where geology is geopolitics. Control of the periodic table is now as decisive as control of sea lanes or satellite constellations.

China throttles rare earth exports, weaponizing its near-monopoly in magnets and battery materials. Its Belt and Road Initiative has already secured lithium and cobalt across Africa and South America.

Russia leans into resource nationalism, tying uranium exports and energy corridors to its foreign policy goals. Kazakhstan—producer of over 40% of the world’s uranium—sits in Moscow’s orbit.

India is no longer just a consumer but an aggressive competitor, racing to lock down lithium supplies in Argentina and rare earth projects in Australia.

The West risks becoming a permanent importer, dependent on rivals for the metals that power its grids, weapons, and economies.

This is not about abstract “market dynamics.” It is about whether democracies will control their own futures.

Without uranium, copper, lithium, and rare earth elements, there is no AI revolution, no data center backbone, no renewable transition, no electric vehicle fleet. Strip away the minerals, and the high-tech towers of modernity collapse like sandcastles in the tide.

And here lies the hard truth: exploration is the first act of sovereignty. Mines take 10–20 years to permit and build. If we do not plant seeds now, by the 2030s the United States and its allies will be paying whatever price Beijing or Moscow demands—or doing without altogether.

The call to action is clear:

Reinvest in exploration with the urgency of a Manhattan Project—geological surveys, public-private partnerships, and incentives that pull risk capital back into the field.

Build Western supply chains that can withstand geopolitical shocks, from Nevada lithium to Saskatchewan uranium to Australian rare earths.

Treat geology as strategy, not afterthought. The United States Geological Survey should be viewed with the same seriousness as the Pentagon, for both are guardians of national defense.

This is the rallying cry for the U.S. and its allies: sovereignty begins at the drill rig. Without exploration, there is no mining. Without mining, there is no economy. Without an economy built on secure foundations, there is no freedom to defend.

A Glimmer of Policy Reform

For all the gloom, there are sparks of recognition—early shoots that hint the field may not be barren forever.

FAST-41 Permitting Reform: Once a bureaucratic chokehold, permitting in the U.S. is showing signs of movement. The Federal Permitting Improvement Steering Council (FAST-41) is beginning to streamline timelines for “covered projects.” Uranium juniors like Anfield Energy with its Velvet-Wood mine in Utah, and EnCore Energy with Dewey-Burdock in South Dakota, have already secured wins under this process. What once looked like stranded assets are edging toward daylight.

Pentagon–MP Materials Partnership: The U.S. Department of Defense has invested directly in MP Materials’ Mountain Pass rare earth mine in California—hundreds of millions of dollars in contracts to secure separation and magnet manufacturing capacity on U.S. soil. This is no boutique project: MP Materials controls the only rare earth mine (of scale) in the U.S. and is ramping toward vertical integration that could anchor a Western supply chain.

Copper as a Keystone: Projects like Resolution Copper in Arizona—one of the largest undeveloped copper resources in the world—remain politically tangled, but their scale makes them unavoidable. If unlocked, Resolution alone could supply up to 25% of U.S. copper demand for decades.

Lithium Rising: The controversial but progressing Thacker Pass project in Nevada, and Ioneer’s Rhyolite Ridge, have secured federal loans and partnerships, positioning the U.S. as a serious player in lithium carbonate production. Thacker Pass, with more than $2 billion in projected investment, is not just a mine but a downstream refining hub in the making.

Downstream Momentum: Supply chains are finally catching political attention. From rare earth magnet plants in Texas to lithium hydroxide refineries in Nevada, the U.S. is beginning to invest not only in the rocks, but in the capacity to turn them into finished products. That is the true measure of sovereignty.

These reforms are encouraging, but they are still small strokes on a canvas that demands bold, sweeping lines. A handful of permitting wins and defense contracts are not a revolution. What’s needed is a scale-up—tenfold, a hundredfold. Only when the U.S. and its allies treat minerals with the same urgency once reserved for oil, or for the space race, can we say things have truly changed.

This glimmer is fragile, but it is real. If fanned, it could light the torch of a new exploration renaissance.

Conclusion: Choose Risk or Embrace Ruin

The mining industry thought it was playing it safe by pulling back on exploration. In truth, it was gambling the future—trading short-term stability for long-term scarcity. The result is hollow pipelines, fragile supply chains, and a generation of geological knowledge at risk of fading into silence.

Exploration is not a luxury. It is the R&D of civilization itself. Without it, there is no copper for wires, no lithium for batteries, no uranium for baseload power. Starve exploration, and we starve the future.

The real risk isn’t in drilling holes—it’s in failing to drill them. The world’s faucets are running, but the reservoir is dropping. The only question that remains is whether we have the vision and courage to dig the next well before the water stops.

For those still with me at the end of this essay, here’s the wry truth in one line:

“Exploration: the riskiest bet we can’t afford not to make.”

The bedrock just shifted — and not because of tectonics.

MP Materials, the sole U.S. producer of rare earth elements, has inked a $400 million deal with the Department of Defense. The investment cements the Pentagon as its largest shareholder and catalyzes a deeper realignment of America’s critical minerals strategy. But this isn’t just a finance story — it’s a geological one, a strategic one, and potentially a transformational one.

Let’s crack it open.

From Mountain Pass to Magnet Hubs: Rebuilding a Domestic Value Chain

The heart of this deal is vertical integration. MP Materials will use the funding to construct a second magnet manufacturing facility — dubbed the “10X Facility” — bringing total planned U.S. magnet output to 10,000 tonnes per year by 2028. Meanwhile, the Mountain Pass mine in California, already a rare example of integrated mining and refining, will undergo a major upgrade to process heavy rare earths, a capability that’s currently nonexistent within U.S. borders.

Together, these efforts represent the scaffolding of a fully domestic mine-to-magnet supply chain — a national security asset in its own right, with magnets destined for F-35s, EV drivetrains, satellites, and hypersonic missiles alike.

The Pentagon isn’t dabbling here. This is a decade-long offtake agreement, a price floor of $110/kg for NdPr, and a $1B private financing commitment to ensure downstream buildout. It’s the kind of market-making intervention that turns a company into a cornerstone — and an industry into a priority.

A Signal to the Mining Sector: This Is Industrial Policy in Action

For those of us swinging hammers in the field and flipping core trays in the trailer, this deal resonates loud and clear: Critical minerals are no longer just a speculative asset class. They are now the subject of coordinated national policy.

This move sets a precedent. The government isn’t merely supporting production; it’s underwriting it — mitigating price risk, anchoring demand, and becoming a shareholder in the supply it wants to see developed.

That playbook doesn’t end at rare earths. Expect copycats — or cousins — across lithium, cobalt, niobium, tellurium, and even uranium. The message is: if it feeds national defense, the energy transition, or technological sovereignty, the U.S. is now willing to back it with more than words.

For geologists and explorers, this means:

Increased funding for early-stage discoveries in critical mineral belts.

Stronger pull-through for domestic projects that show scale, purity, and ESG performance.

More favorable permitting conditions when aligned with national goals.

A growing appetite for substitutes and analogues — think heavy REEs outside China, battery materials outside Congo, or even thorium and scandium as byproducts.

Pathfinders in the Radiogenic Shadows: Thorium, REEs, and the Exploration Model

The Mountain Pass model — carbonatite-hosted rare earths with a radioactive signature — remains one of the most studied (and still underutilized) exploration templates in North America.

Thorium, often treated as a nuisance, is actually the glowing breadcrumb in the geochemical hunt for similar deposits. Mountain Pass was identified in part because of elevated thorium readings during postwar radiometric surveys — a technique that’s ripe for revival with modern tools.

Imagine reanalyzing old radiometric surveys across the Basin and Range or Rockies with a critical minerals lens. With airborne gamma spectrometry, machine learning, and hyperspectral satellite data now at our fingertips, we’re not just walking old ground — we’re re-seeing it.

This deal should reignite interest in:

Thorium pathfinder anomalies in alkaline systems and pegmatites.

Heavy REE-enriched districts in Wyoming, Texas, and Alaska.

Tailings and waste rock with underexplored critical mineral content.

REE byproducts in carbonatite-associated copper or phosphate systems.

Mountain Pass wasn’t a fluke — it was the result of recognizing radiogenic clues and metallogenic context. We have the maps. We have the data. What we need now is the will.

What’s Downstream is Upstream’s Business Now

This is a case where downstream developments — like magnet manufacturing — change the calculus upstream. With the Pentagon as a guaranteed buyer and long-term partner, magnet supply chains gain the financial predictability needed to invest in innovation, expansion, and diversification.

And that demand rolls uphill.

Copper miners could find offtake markets for dysprosium or terbium as trace byproducts.

Phosphate producers may re-evaluate their monazite waste streams.

Uranium explorers, especially in thorium-rich systems, might start looking at REE recovery circuits.

Industrial mineral companies, often ignored, could become critical suppliers if they sit on the right fluorite, barite, or bastnaesite-hosted systems.

Where once there was only risk, now there is signal — a big, bold signal saying Build it here. Mine it here. Sell it here.

Final Thoughts: A Turning Point for Geologists, Not Just Manufacturers

This MP–Pentagon deal is more than capital infusion — it’s a tectonic affirmation of our industry’s relevance. It says that what we explore, discover, and extract matters not just economically, but strategically.

We’re used to asking: “Is this deposit feasible?” Now we also get to ask: “Is this deposit vital?”

And the answer, more often than not these days, is yes.

So as rare earths take center stage and thorium-laced anomalies begin to glow again in the collective memory of the geological community, the message is clear: The drill rig is back in fashion — not just in markets, but in national strategy.

And that, my friends, is worth staking some ground for.

— Mark Travis, CPG Founder, Arkenstone Exploration Writer, Rock Whisperer, Advocate for the Sacred Duty of Discovery

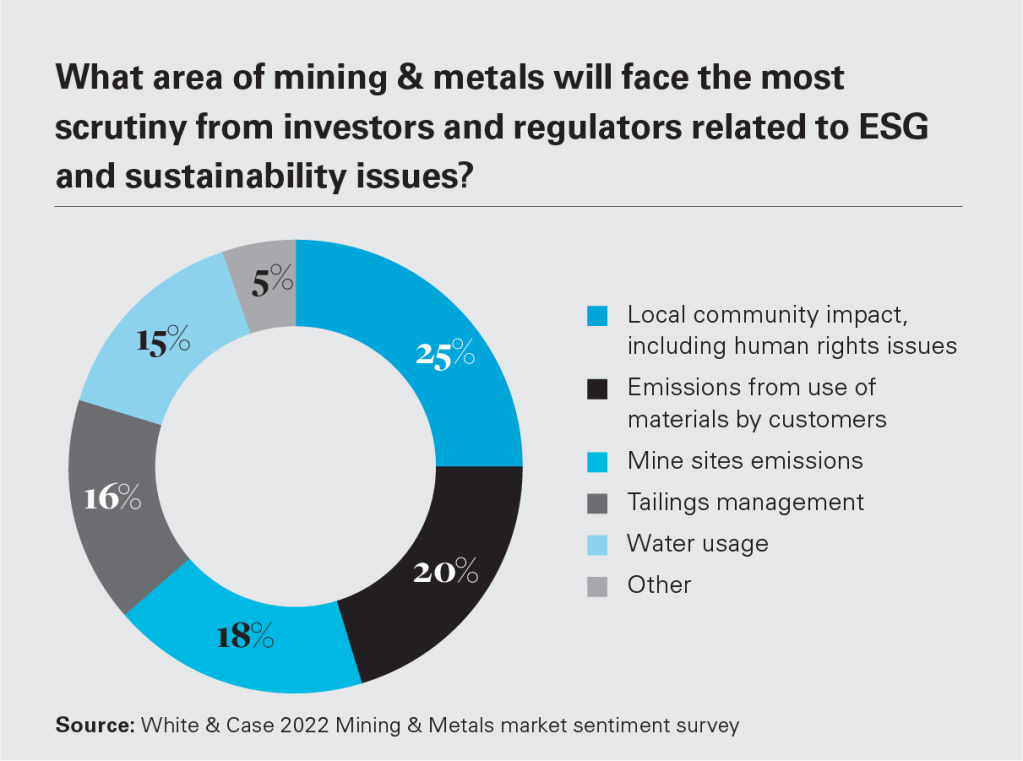

The electrification transition, aiming to shift dependence from fossil fuels to electricity, brings a surge in demand for minerals crucial for batteries, renewable energy infrastructure, and electric vehicles. In addition, the nascent small modular reactor (SMR) industry will carry much of the heavy lifting to replace coal-fired power plants with factory built nuclear reactors. This has significant implications for the mineral exploration industry, where Environmental, Social, and Governance (ESG) factors are gaining increasing importance. However, without an overhaul of current permitting processes in countries like the USA, these transitions will be greatly stymied if not completely deferred to jurisdictions that are agile enough to pivot in the face of a changing landscape.

Environmental:

Mining Activities: Exploration and extraction can cause environmental damage through land disturbance, water pollution, and greenhouse gas emissions. But this needn’t be true if that mining is conducted within jurisdictions where sustainable, clean, and regulated mining activities prevail. Companies are expected to minimize these impacts through responsible practices, like using renewable energy sources, mitigating water usage, and implementing effective land reclamation strategies. But most current mining for critical minerals and minerals needed for the electrification transition are happening in areas with little to no oversight or safe-guards for the environment.

Climate Change: The electrification transition aims to combat climate change, but mineral extraction itself can contribute to emissions. Companies need to demonstrate clear strategies to reduce their carbon footprint and operate sustainably throughout the value chain. One such avenue would be to use SMRs to provide carbon-free base-load power from nuclear power sources that can feed into electrically-powered fleets on the modern mine site. In this way mineral extraction could close the loop on electricity and mineral production achieved in a wholly carbon-less capacity. But this would require leaps and bounds in both permitting prowess and investor willpower.

Social:

Community Engagement: Exploration often occurs in remote areas with existing communities. Companies must engage with these communities transparently, respecting their rights and cultural heritage, and ensuring fair benefit sharing. Within the current framework here in the USA these systems have been in place for decades. However, self-serving NGOs that label themselves as ‘environmentalists’ find ever-unique ways to obstruct and corrupt a well-meaning regulatory system that provides better protections than anywhere else on the globe. All while China continues to forego any of these considerations to produce the consumer products we here in the West enjoy without a second thought.

Indigenous Rights: Indigenous communities may have specific rights and interests in the land where exploration takes place. Companies need to consult and collaborate with them throughout the process, respecting their rights and traditional knowledge. Many of these communities are able to provide a wealth of knowledge on how best to care for the land and nurture the native plants that must be protected.

Labor Standards: The mining industry has a history of labor abuses. Companies are expected to uphold fair labor practices, ensuring safe working conditions, living wages, and equal opportunities for all workers. On the modern stage of diversity and inclusion, today’s face of mining looks drastically different than those images found in Gold Rush museums and Prospector’s journals of a bygone era. Women in mining are having their day and this bulwark will continue to grow.

Governance:

Transparency and Accountability: Investors, communities, and other stakeholders are increasingly demanding transparency from mining companies regarding their ESG practices. Companies need robust reporting systems and accountable governance structures to demonstrate their commitment to sustainability. But ultimately, the narrative needs to change from one of villainy towards an understand that ‘minerals are life’ and each human life requires a certain base-amount of minerals to be extracted in order to sustain that life.

Regulations and Licensing: Governments are implementing stricter regulations to ensure responsible mining practices. Companies need to comply with these regulations and actively participate in shaping responsible mining policies. But more importantly, the regulatory agencies need to provide a clear path forward for companies and investors alike towards achieving extraction of the sorely needed mineral resources.

ESG and the Electrification Transition:

Responsible Sourcing: As demand for battery minerals like lithium, cobalt, and nickel increases, ensuring their responsible sourcing is crucial. Other minerals such as uranium, copper, silver, REEs, and many others will have a part to play in the coming dance for mineral extraction. Companies need to partner with suppliers who adhere to high ESG standards throughout the supply chain. And mid-stream processing and enrichment of extracted minerals need to feed the manufacturing industries on the self-same soil that the minerals were extracted. At this time, most raw material processes needs to circumnavigate the globe before it can be used to make anything.

Social License to Operate: Communities and stakeholders are becoming more vocal about the social and environmental impacts of mining. Companies that fail to uphold ESG standards risk losing their social license to operate, hindering their ability to access critical resources. However, the segmented nature of various mining activties divorce the outcry from the ability to impact the end product. In other words, it is nice to decry mining’s ill from the USA while having no direct impact on mining’s impact within China where these criticisms fall on deaf ears and have no real impact. After all, these are completely different nations.

Investor Scrutiny: Investors are increasingly integrating ESG factors into their investment decisions. Companies with strong ESG practices are likely to attract more investment and have a lower cost of capital. But even after nominally identifying the correct company, jurisdiction, or geologic setting, the regulatory hurdles to opening the doors at any “perfect mine” are still quite high and flanked by obstructionist NGOs that care little for the environment they claim to protect and more about the misguided, out-dated narrative they continue to espouse.

In Conclusion: ESG considerations are no longer optional for mineral exploration companies in the electrification transition. But understanding the challenges that mining companies face in this tumultuous terrain needs to be taken into consideration as well. By prioritizing responsible practices, companies can mitigate risks, secure community support, attract investors, and contribute to a sustainable future for the industry and the planet.

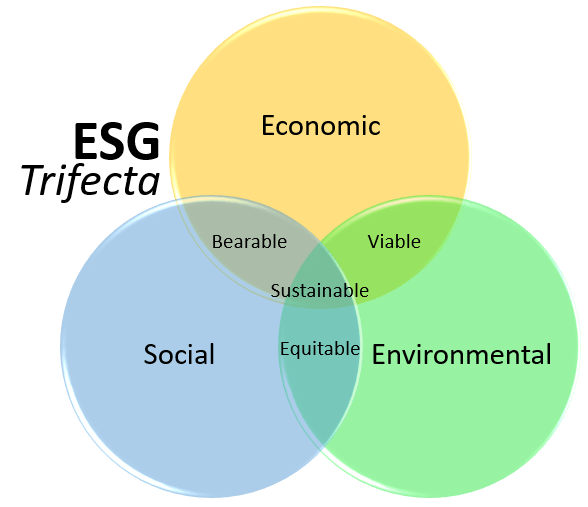

There is a global shift to the domestic production of minerals. This is happening across the world and is having ripple effects both up stream and down stream in this forward looking economy. It might seem somewhat backward to look inward for stable economic pillars for the global economy. But I might argue the opposite in the face of the ESG (economic social governance) paradigm we, as a species, seem to be self-implementing in this post-pandemic world. It is a natural step to draw from domestic natural resources, should we want to have a greater say in how those resources are produced. It might be the hallmark of the Dotcom boom that most of the materials that built it came from a supply chain wholly opaque to the consumer. And perhaps that system was built with the exact purpose of keeping such machinations obscured from the public eye. Nonetheless, it is perhaps an outdated mode given the current global climate. Imagine the backlash in today’s global economy. Imagine if all companies adhered closely to the transparent ESG paradigm.

As a quick re-cap, the Environmental/Social/Governance paradigm is a global movement for business to be conducted in a transparent way that responds to the socially responsible investor. But in reality it is a current day risk mitigation that takes into account “non-financial” factors when assessing sustainability. In a mineral industry context, the days of a mine’s sustainability equaling its mineral resource or mine life is long past. In truth, this reality has been long-coming and began decades ago here in the U.S. with NEPA (National Environmental Policy Act, 1970). While NEPA is a laudable step towards sustainability, it’s main problem is it’s scope; it only affected the U.S. In short, NEPA was one step forward, two steps back for domestic production of minerals here in the U.S. While the U.S. implemented what is known today as the “NEPA process” other jurisdictions, such as China or Russia, continued business as usual. In this way, the U.S. has continually become less a producer and more a consumer, not only when it comes to mining but across all sectors.

Why does this shift matter? And how could this global transparency and awareness bolster a budding domestic mineral industry? In a way, the ESG paradigm could be harnessed to level the playing field between the un-regulated, “Wild West” mineral producers and the well-regulated non-producers.

We stand at a crossroads. Should the U.S. source it’s resource needs from within or continue to push the social/environmental liability elsewhere? If COVID taught us anything, global supply chains can be swiftly eroded and being self-reliant, even within an ever-expanding global economy, will pay dividends. And in the context of the socially responsible investor & ESG, we should all be able to pull the veil back and see exactly how the sausage is made.

In the Kingdom of Saudi Arabia, as part of their Vision 2030 initiative, they are pivoting towards a future that is diversified to include domestic production of green metals, energy metals, and other precious & base metals production. The Kingdom is most obviously known for its hydrocarbon production, but there is a long history of gold and copper production as well. The Arabian Shield is geologically very old and host to untold riches that have yet to be exploited. In fact, the USGS during the 1950s thru 70s had numerous field mapping campaigns to try and encapsulate these resources outside of the scope of oil & gas.

If a key player within the supply of current fuels has the wherewithal to begin to pivot towards the future, surely the U.S. can find the backbone to do the same. But there is one question that would need to be answered before that could happen: Can we reconcile the fact that, in order to build the green future of the electrification transition, we will need to mine minerals? Current policy from the Biden administration seems keen to promote domestic production of minerals but actual investment from the Dept of Defense is looking beyond our borders to non-domestic mineral resources. This is quite discouraging given the vast endowment of natural resources the U.S. already has within its borders.

I’ve seen this bumper sticker, found in many a mining town, that goes something like: “If it’s not grown… it’s mined.” There’s nothing like some bumper sticker wisdom to solve any problem, right? Seriously though, this might seem like an over simplification of a complex problem, but is it? Resources, by their very definition, are something that must needs be exploited. Now. This exploitation can be done ethically, with all stakeholders at the table, or we can continue to allow other countries to do our dirty work for us. In short, if we don’t mine it cleanly (per our own NEPA regulations) then someone else will mine it however they see fit (without regulatory oversight, most likely). To be honest, unregulated mining is the most profitable (for the mining company)… that’s why it was done that way historically. So then, what is the point of ESG (or any set of standards, for that matter) if we are not all playing by the same rules?

The domestic production of minerals (aka, mining) is ultimately the logical conclusion of the green energy thought experiment. Don’t shoot the messenger when you find out that in order to transition away from carbon you will need to invite some other elements to the party. As Hunter S. Thompson encapsulated so eloquently, “Buy the Ticket… Take the Ride!” If the goal is to electrify our energy and transportation sector by means of transitioning away from carbon sources of fuel, then the only alternative is a suite of other elements/minerals. These minerals have be enumerated in the critical minerals list put out by the USGS. And here is the good news: all of the elements found on the critical minerals list can be found here within the U.S.

It’s no secret to those who’ve been paying attention. Minerals equal life. And in order to produce said minerals, they must be mined. The only true debate left is when, where, and how. When will we start to mine these minerals that are required to move forward? Where will we decide to mine these minerals so we can have a say in how they are produced? And how will we do so in an ethical, socially responsible, and sustainable way?

It’s not a giant feat by any stretch. Many of these questions can be answered by visiting your local phosphate, lithium, copper, or gold & silver mine found thought out the Western U.S. They have been quietly producing these vital minerals for decades. The problem now, of course, is there are precious few of them opening up anew. Many of these deposits have a long, battle-worn history of achieving the hard-won state of “in production,” and perhaps rightly so. But it’s it about time we found a more cooperative solution to guiding the mineral producer through the NEPA process and onto actual mineral production. I can see more opportunities to help the miner and the conservationist alike through cooperative permitting. But that sort of “kumbaya” moment doesn’t make for sexy headlines for the 24 hour media cycle to sell. And few environmental activist firms would be able to set up shop with that kind of business model.

The US has a challenge to face: balancing regulatory oversight with mineral needs and the ability to realize those needs in our backyard.

The US has ample critical minerals, precious metals, base metals, and other natural resources needed for the electrification of the energy and transportation sectors. The US also has robust regulatory oversight and a permitting process (NEPA) that, in theory, should provide a predictable, timely path for a deposit to become a mineral asset for the electrification transition. This is, of course, based on the assumption/need to decarbonize the energy and transportation sectors. In this light, it is a potentially bi-partisan, progressive issue that could provide many collaborative ‘win-wins’. However, in reality this has failed to play out.

The mineral industry across the US has experienced, instead, a protracted permitting process troubled with last-minute changes, litigation, and back-tracking of previously made decisions. This is unsustainable within an industry that already endures a 10 year permitting process whereas other nations with similar environmental laws are seeing this done in a 2 – 3 year window. Current worse case scenarios are seeing permits taking 15+ years with hundreds of millions of dollars spent to only have it all taken away with last-minute, frivilous litigation and back-tracking.

Recently, the US military has been looking to invest in Canadian mining projects, banking on the fact that US permits are more risky than investing in “friendly” neighboring countries. US tax payers are seeing their tax revenue spent to bolster other nation’s mineral wealth. It would be better to keep that money here locally and invest in our own home-grown natural resources. It is a true indictment of our US permitting process when the US military is strategically investing across the border instead of on our own soil.

How can we find common ground and opportunites to mutually benefit from critical mineral production?

Current legislation, such as the Infrastructure Law, CHIPs and Science Act, & the Inflation Reduction Act, are collectively providing $135 billion to build the US electric vehicle future, including critical mineral sourcing and processing and battery manufacturing. And most recently, on October 19th, the White House announced $2.8 billion in grants for domestic critical mineral projects.

So, there is money available, but will mineral projects be able to capitalize on these opportunities in time? There is money available, but will that money actually reach the ground where it is needed? Only time will tell as more often than not the exploration and mineral sector is subject to the whims of one political administration to the next and the already cyclical nature of the sector also has to pay attention to the 4 year election cycle as well.

Nonetheless, the NEPA process already has some baked-in streamlining with MOUs between key federal agencies that in theory provide for non-duplicative work when reviewing a permit. But this is not always followed or policed by a lead agency. And this isn’t helped either by the venture capital markets that tend to bring in outside money from Australia and Canada into the Western US. There are few and far between US-based mining companies and even less of these companies are actively exploring for the next generation’s mineral wealth.

This is a long-term, systemic problem that comes from a simple truth about the mineral industry: a single deposit will be owned by, explored by, & peddled by numerous companies over numerous cycles before it may ever see actual production. These mineral deposits have to run the gaunlet of economic cycles, political cycles, commodity-needs cycles (one cycle’s trash is the next cycle’s treasure), as well as benefit from sound exploration geology to expand upon known mineralization. It doesn’t help if on top of all these systemic challenges the permitting process has become increasingly mired in special interest and unpredictability.

Is it time to play the long-game like China?

Our global competition for these minerals and the ability to process them and make a useful end product is very stiff. China has out-paced and out-performed the US at every turn, all while we continue to be grossly reliant on their mining and manufacturing prowess. We are a consumer nation with little production to call our own. How will we fare if relationships abroad continue to sour? Where will we turn for our resources if we haven’t invested in our own backyard?

China is able to play the long game. They can see the long-term worth in something, take a loss on the project for years, in order to realize long-term gains decades from when they began the project. Where is our will as a nation to come together on such projects? This sort of longview is impossible if we can only plan as far as the next election cycle.

Setting these myriad global/political issues aside we need to come together as an industry, as a nation, and as a people to find common ground between ideological difference. The US can truly benefit from sourcing our mineral needs from within our borders. And no one need lose out in the process. We have the resources, the regulations, and the self-determinating spirit. If we stopped wasteful in-fighting and educated ourselves and the public about our home-grown natural resources we could realize true wealth here in the US.

Here in the US we are blessed with both a rich mineral endowment and robust environmental regulations. However, these two forces that ideally could work together to create a more perfect mineral industry are instead at odds with one another through a series of unfortunate ideological mis-steps. There is no doubt that legacy mining efforts here in the Western US have left many areas in need of proper reclamation and clean-up, to say the least. But what the environmental movement chooses to forget is that many of these problems were created prior to the NEPA process and our robust regulations. So while the US minerals market struggles to navigate modern mining within favorable geologic settings other nations, such as China and Russia, continue to exploit their minerals, and those of other nations, unimpeded and without any true oversight of their methods. This has created a huge misdirection of efforts to provide the modern world with much needed mining while also conducting this mining in a clean and efficient manner. Here in the US we can boast robust environmental regulations, yes. But we can’t boast a robust mining sector that provides for our mineral needs. We have pushed much of that burden elsewhere and continue to ignore the very real environmental harm done by global mining efforts.

How do we balance this disconnect? How can we re-patriate our mineral needs while also adhering to our robust regulations? This step needs to happen while we still have time. The US, now more than ever, needs to find cooperative ways to satisfy two seemingly opposing forces: mineral needs and the environment. If you are reading this on a computer, smart phone, or even on paper contemplate the minerals and industrial processes that went into bringing you these words. We, as humans, impact the very earth we stand upon each day without much thought put behind our every actions. The amount of minerals required for each person to thrive in this world is greater than most might realize. And so we need to educate ourselves and others about these realities and then find creative solutions to meet these needs here at home. An ounce of local stewardship of our natural resources will be worth more than the pound of consumerism culture the US has become in modern times. We spend more money pushing the environmental impact of our actions onto other nations when we could have instead realized that growth and benefit for ourselves here in our own backyard.

So the challenge becomes an ideological one, not a physical one. We have the minerals, the raw materials to build the bright future available to us all. With the rise of EVs, solar power, and the electrification of our world we will require more and more minerals each year. If the goal is to move away from carbon sources of energy then minerals are the only alternative. This means more mining and more infrastructure required upstream to process these raw materials into products, materials, and energy. But this challenge is won or lost before the first drill rig is mobilized or the first ton of dirt moved. This challenge needs to have buy-in from all stake-holders.

The mineral explorationist needs to see how their actions impact later generations just as much as the environmentalist needs to realize how their obstruction simply pushes the impact onto other jurisdictions. If this mineral production is not done in our own backyard it will be done somewhere else without the oversight our regulations provide. And in the process we will lose out on the economic benefit that comes from producing our own materials for our own needs. The need won’t go away. Humanity will continue to grow. Our only choice is whether or not it will thrive.

So how should we proceed? What lessons can be learned from the past? The paradigm of ‘us vs. them’ needs to be set aside. There are so many opportunities for cooperative development in the world of mineral development. Many of the issues that are decried by the geologist and environmental activist alike could be addressed through responsible mining of the critical minerals needed to build our modern society. For example, many of the legacy mine sites that require reclamation and clean-up still hold many of the critical minerals we need to produce. The most cost-effective way to clean-up these sites is thru active mining. This may seem counter intuitive but it is true. The money generated by active mining would easily pay for the clean-up required. Typically, the chemicals that are contaminating the aquifer or making the soils toxic are directly associated with the critical minerals that need to be produced. Cooperative efforts such as these could help heal the divide between these seemingly opposing groups.

But perhaps such simplistic and naïve hope belies the more realistic forces at work today. Perhaps none of these groups are here to be good stewards of our nation’s mineral endowment. For one, there are few and far between US-based mining companies. The vast majority of the venture capital that makes it to our shores comes from either Canada or Australia. We, as a nation, have forgotten what it means to own and produce our own resources. Instead we have become consumers rather than producers. And then on the other hand, environmental activism is rarely as altruistic as it might seem. These environmental groups rarely go after the mining company themselves. Rather, they litigate with the regulatory agency that issued the permit to explore or mine. They attack the very agency that is doing their work for them and then the agency settles this litigation by paying them off. Thus the obstructionist engine is fueled. Allowing them to find the next species or special interest in need of protection.

This model is unsustainable. If we prioritize mineral production in our backyard we can lead by example. We can realize the rich mineral endowment of the US while also implementing our environmental regulations. This is a true ‘win-win’ that can illustrate our values of self-sufficiency and good stewardship. The alternative is more in-fighting and continued regression into a consumer culture that is blind to the sources of the things we consume. I’d like to say the choice is ours, but realistically these forces are beyond the reach of most of us. The best we can do is to stay educated and strive to educate others. Awareness and intelligent debate will have to take the place of true power until there is such a ground swell to progress past the old ‘us vs. them’ paradigms that the global forces in play choose cooperative compromise in order to realize the bright future already laid out before our feet.