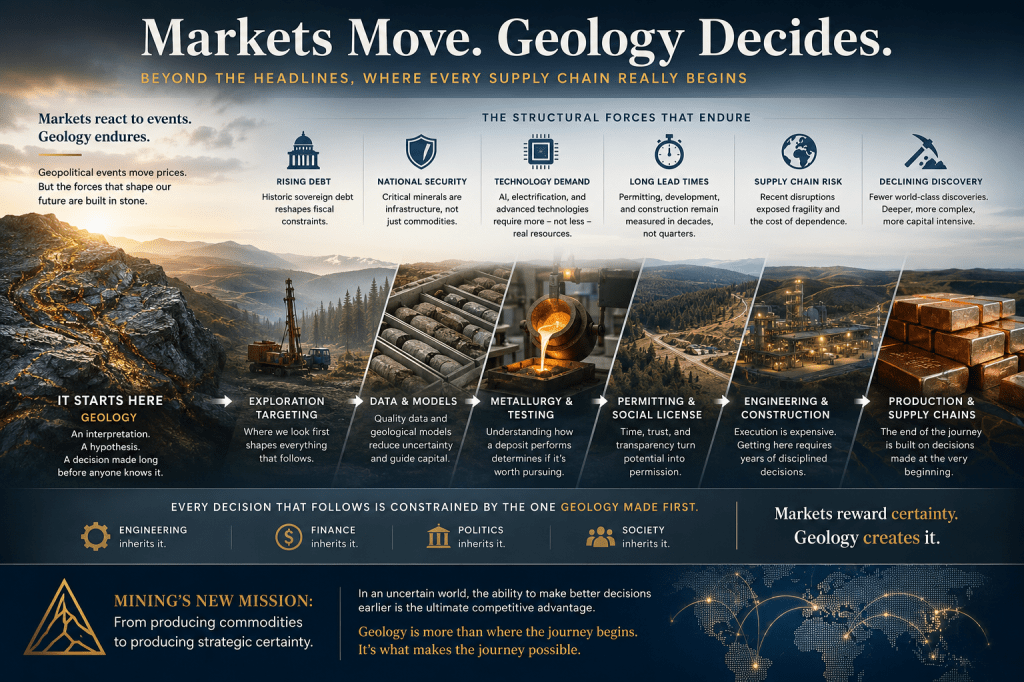

“Markets react to events. Geology endures.”

Markets Move. Fundamentals Don’t.

Markets have a remarkable talent for mistaking motion for change.

Every session brings repriced risk, rewritten narratives, and fresh declarations that a new era has begun — or ended. Commodity prices surge or collapse. Analysts race to explain every tick. Investors scramble to determine whether this time is truly different.

Then the moment passes.

Oil retreats. Gold surrenders its safe-haven premium. Silver softens. Equities recover. The headlines move on.

The conclusion seems obvious: geopolitical tension briefly inflated commodity prices before markets returned to normal.

I’d argue something quite different.

The markets moved. The fundamentals didn’t.

Many of the forces that have drawn investors toward commodities over the past several years haven’t merely persisted — they’ve quietly strengthened. Sovereign debt remains at historic levels. Nations continue pouring capital into defense, energy security, artificial intelligence, electrical infrastructure, and the domestic industries required to support them. Mine permitting timelines are still measured in decades. New discoveries keep getting deeper, more complex, and more capital-intensive, even as the number of truly world-class finds declines.

None of that changed because the risk premium faded.

If anything, the recent conflict served as a reminder of how interconnected — and how fragile — global industrial supply chains have become. It didn’t create those vulnerabilities. It exposed them.

That distinction matters. Because the Iran conflict may ultimately be remembered not for the commodities it temporarily moved, but for the assumptions it permanently challenged.

A Different Kind of Mining Cycle

For decades, mining has been understood primarily as a cyclical business.

Prices rise and fall. Exploration booms and busts. Capital floods in during bull markets and retreats when sentiment turns. The pattern has repeated often enough that most investors assume today’s correction is simply another turn of the same wheel.

But what if the wheel itself is changing?

A quieter transformation has been unfolding beneath the surface — one that rarely competes with commodity prices or quarterly earnings for attention. It has emerged gradually, embedded in exploration releases, government policy, supply chain disruptions, and shifts in how capital is allocated. Individually, these developments appear unrelated. Together, they point somewhere new.

Governments increasingly treat critical mineral projects as matters of national security, not conventional industrial development. Major miners are no longer focused solely on replacing reserves — they’re working to secure entire supply chains. Capital has grown more selective, rewarding projects that demonstrate not just strong geology, but credible permitting pathways, processing solutions, jurisdictional stability, and long-term strategic relevance.

Even the language of the industry has changed.

Not long ago, mining conferences revolved around grades, strip ratios, recoveries, and commodity forecasts. Today’s conversations center on domestic manufacturing, downstream processing, supply chain resilience, and strategic independence.

These aren’t buzzwords. They represent a fundamental shift in how society assigns value to geology itself.

Ironically, this transformation has arrived precisely when portions of the market appear to be losing interest.

As gold and silver retreat from recent highs, some investors read lower prices as evidence that the long-term thesis has weakened. I see something different.

Markets have always been good at pricing today’s fear. They are far less capable of recognizing tomorrow’s constraints.

Reduced fear is not the same as reduced risk.

A falling gold price doesn’t build a new copper mine. A softer silver market doesn’t shorten a fifteen-year permitting timeline. A temporary easing of geopolitical tension doesn’t conjure domestic rare earth processing capacity where none existed before.

The structural challenges remain exactly where they were before the first missile was launched. If anything, governments now have a sharper appreciation of the consequences of ignoring them.

Which is why the most important story in mining today isn’t about commodity prices at all. It’s about how decisions get made — and where they truly begin.

Where Every Supply Chain Actually Starts

Every significant decision begins long before anyone recognizes it as a decision.

Long before a board approves a billion-dollar mine. Before governments negotiate strategic mineral agreements. Before engineers design processing plants or investors debate project valuations.

Every major mining project begins with an interpretation.

A geological model. A structural hypothesis. An understanding — sometimes incomplete — of how nature assembled a mineral deposit over millions of years.

Everything that follows inherits the quality of that initial understanding. Capital allocation. Exploration targeting. Metallurgical testing. Resource estimation. Permitting. Engineering. Construction. Even national supply chains ultimately inherit the possibilities — and the limitations — established by those earliest geological decisions.

Engineering doesn’t create those possibilities. Finance doesn’t create them. Politics doesn’t create them.

They inherit them.

Geology made the first decision.

That reality has always existed. What has changed is our appreciation of its importance.

For much of the past generation, globalization allowed developed economies to treat geology as someone else’s problem. Metals could be sourced wherever they were cheapest. Processing migrated offshore. Supply chains stretched across continents. Efficiency was the overriding objective.

The events of recent years — pandemics, energy crises, trade disputes, geopolitical conflict — have steadily dismantled that assumption.

Resilience is valuable again. And resilience begins at the source: with understanding where critical resources exist, how they can be developed responsibly, and whether they can realistically reach production before the next disruption arrives.

Mining no longer exists simply to produce commodities. Increasingly, it exists to produce strategic certainty.

That is a very different mission — and it may prove to be the defining characteristic of the next generation of this industry.